You will need to calculate your month-to-month funds on your federal loans to know how a lot revenue you might want to carve out on a month-to-month foundation on your pupil loans. For those who really feel like your fee is simply too excessive, try the income-driven choices. These might be fairly inexpensive, significantly for newly graduated debtors, for these in a coaching program, for these dropping hours, or for these getting into the workforce after a hiatus.

We created this calculator to assist simulate your month-to-month funds. If it reveals a clean display screen or no calculator is listed, simply refresh the web page.

Enter your mortgage quantity, rate of interest, revenue, and family measurement to generate your month-to-month fee throughout the federal compensation plans.

*This calculator is assuming the borrower is single or submitting taxes as a pair married submitting collectively. For those who’d wish to run the numbers as a pair married submitting individually right here’s our useful resource or rent one in every of our pupil mortgage execs that will help you run the numbers

Wish to obtain the calculator? Fill out the under and also you’ll obtain a hyperlink to the calculator and subscription to our month-to-month publication.

How you can Estimate Pupil Mortgage Compensation

For those who’re the DIY kind and wish to calculate the month-to-month fee with pen and paper or by means of a spreadsheet, right here’s what you might want to know. Discretionary revenue (DI) is used to calculate your month-to-month fee within the varied IDR plans.

- Commonplace Compensation Plan – mounted funds over 10 years

- Graduated Compensation Plan – funds begin at a decrease quantity and improve each two years at a price to repay the mortgage over 10 years

- Prolonged Compensation Plan – mounted funds over 25 years

- Prolonged Graduated Compensation Plan – funds begin at a decrease quantity and improve each two years at a price to repay the mortgage over 25 years

- Earnings-Pushed Compensation (IDR) Plans – funds are calculated as a proportion of discretionary revenue. IDR plans are a requirement for Public Service Mortgage Forgiveness (PSLF).

Commonplace compensation plan

To calculate month-to-month funds in the usual compensation plan is sort of easy: plug the numbers right into a mortgage calculator on-line or on the calculator on this web page.

Inputs

- Rate of interest = 7%

- Mortgage Time period = 10 years

- Current Worth (mortgage stability) = $200,000

Right here’s the formulation

=PMT(7%/12,10*12,200000,0,0) = $2,322

Graduated compensation plan

Calculating month-to-month funds within the graduated compensation plan is tougher than for the usual or prolonged choices. Funds will often begin out about ½ of what funds are in the usual 10-year compensation plan. Each two years, funds will improve. On the finish of compensation, funds may very well be 1.5x what funds are in the usual 10-year compensation plan.

Month-to-month funds based mostly on the instance above could be ~$1,166.

Prolonged compensation plan

To calculate month-to-month funds within the prolonged compensation plan, you comply with the identical course of you do with the usual compensation plan for all the things besides the time period:

Inputs

- Rate of interest = 7%

- Mortgage Time period = 25 years

- Current Worth (mortgage stability) = $200,000

Right here’s the formulation

=PMT(7%/12,25*12,200000,0,0) = $1,413

Earnings Pushed Compensation Plans

IDR plans are calculated in another way than the three compensation plans mentioned earlier. Funds are based mostly in your revenue and family measurement. Your month-to-month fee is calculated by taking your revenue and subtracting it by the poverty guideline based mostly in your family measurement. This offers you discretionary revenue. Then, based mostly on the IDR plan you choose, it is going to take 10%-20% of your discretionary revenue to calculate your month-to-month fee.

SAVE (previously REPAYE) =Discretionary Earnings = AGI minus 225% of the poverty guideline

PAYE, IBR – Discretionary Earnings = Adjusted Gross Earnings (AGI) minus 150% of the poverty guideline (based mostly on your loved ones measurement and state of residence)

ICR – Discretionary Earnings = AGI minus 100% of the poverty guideline

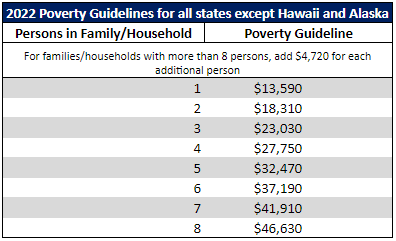

The Division of Well being and Human Companies (HHS) units the poverty pointers. All states besides Alaska and Hawaii comply with the identical poverty guideline which is predicated in your family measurement. Your family measurement is decided by what number of youngsters are in your house, together with any unborn little one who will probably be born in the course of the 12 months. Kids should obtain half of their help from you to be claimed.

Listed here are a few examples as an example how compensation plans can change your fee

Family measurement of two enrolled in SAVE with revenue of $200,000; owes $350,000 @ 7% in pupil loans

- 225% of poverty guideline family of two: 18,310 * 225% = $41,197

- Discretionary Earnings = $200,000 (revenue) – $41,197 (poverty guideline) = $158,803

- Month-to-month Cost in SAVE = 158,803 *10%/12 = $1,323

Family measurement of two enrolled in Outdated IBR with revenue of $200,000; owes $350,000 @ 7% in pupil loans

- 150% of poverty guideline family of two:18,310 *150% = $27,465

- Discretionary Earnings = $200,000 (revenue) – $27,465 (poverty guideline) = $172,535

- Month-to-month Cost in Outdated IBR = 172,535 *15%/12 = $2,157

Family measurement of two enrolled in ICR with revenue of $200,000; owes $350,000 @ 7% in pupil loans

- 100% of poverty guideline family of two:18,310 *100% = $18,310

- Discretionary Earnings = $200,000 (revenue) – $18,310 (poverty guideline) = $181,690

- Month-to-month Cost in ICR = 181,690 *20%/12 = $3,028

Compensation plan choice might be some of the daunting duties if you’re figuring out methods to greatest pay down your mortgage. Right here’s our information on compensation plans.

How Can You Decrease Your Pupil Mortgage Cost?

For federal pupil loans, there are a couple of completely different approaches to decrease your month-to-month pupil mortgage fee.

-Enroll in an Earnings-Pushed Compensation (IDR) plan as a substitute of the usual 10-year graduated or prolonged compensation plan.

–Non-public refinance your federal pupil loans right into a decrease rate of interest. Sometimes, this could offer you a decrease fee.

Strategies to Scale back Month-to-month Funds in Earnings-Pushed Compensation Plans

In case you are already enrolled in an IDR plan and nonetheless wish to scale back your month-to-month fee, contemplate these two methods.

-Contribute to pre-tax accounts, similar to 401(ok)s, 403(b)s, 457s, TSPs, Well being Saving Accounts (HSAs), and Versatile Spending Accounts (FSAs).

-File taxes as a married couple married submitting individually (MFS) – be taught extra about this technique right here.

Sitting down and crunching the numbers might be an eye-opening course of. I do know it was for me after I was figuring out methods to pay down our loans. Simulate your month-to-month funds as quickly as you know the way a lot you’ll be borrowing on your program that will help you establish what month-to-month funds will probably be. For those who’re achieved with college, it’s best to have achieved this yesterday, however as we speak is an efficient time to start out. Having readability in your funds will help you concentrate on the duty at hand whether or not you’re a pupil or busy working skilled. For those who’re struggling about which compensation plan it’s best to choose or confused with methods to start, schedule a time with one in every of our execs

{kind=link}