Federal scholar loans are the most typical sort of loans that college students borrow to finance their schooling. Federal scholar loans ought to be the primary possibility used for undergraduate, graduate {and professional} levels similar to medical faculty. They arrive in quite a lot of mortgage varieties, compensation plans, and mortgage forgiveness choices. Most federal scholar loans are issued at a set rate of interest. Some older loans, similar to Household Federal Schooling Loans (FFEL), had been typically issued as variable price loans.

Right here’s what it’s best to find out about federal scholar loans.

Desk of Contents

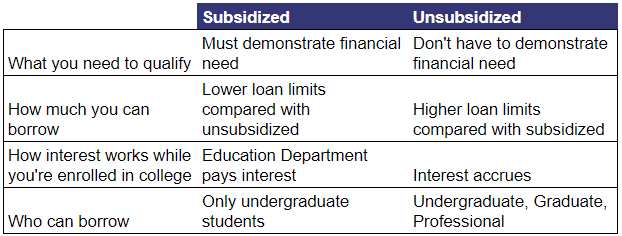

Sponsored vs. Unsubsidized Federal Scholar Loans

Federal scholar loans are provided in two principal classes: backed and unsubsidized. In brief, the distinction between backed and unsubsidized is that direct backed loans have barely higher phrases, similar to decrease rates of interest, and that curiosity doesn’t accrue whereas in class. Since 2012, backed federal loans are solely provided on the undergraduate degree. Anybody pursuing a grad faculty diploma might solely make the most of unsubsidized loans.

Forms of Federal Scholar Loans

There are 5 principal varieties of federal scholar loans to contemplate.

Direct Stafford Loans

Stafford Loans originated from the William D. Ford Federal Direct Mortgage (Direct Mortgage) Program. Direct Stafford Loans are the most typical scholar loans and are at present being issued to assist cowl the price of larger schooling.

There are 3 classes of Stafford Loans:

- Direct Sponsored: Accessible to undergraduates

- Direct Unsubsidized: Accessible to undergraduates and graduate college students

- Direct Consolidation: Accessible to undergraduates and graduate college students

Previous to consolidation, Stafford Loans are eligible for:

Grad PLUS Loans

Grad PLUS Loans, often known as Graduate PLUS Loans, come from the Direct and Household Federal Schooling Mortgage (FFELP) Applications. Debtors are issued these loans to cowl tuition after exhausting Stafford Loans.

Previous to consolidation, Direct Grad PLUS Loans are eligible for:

- Customary Reimbursement Plan

- Graduated Reimbursement Plan

- Prolonged Reimbursement Plan

- All Earnings-Pushed Reimbursement Plans (and PAYE if borrowed after October 1, 2007 and have a federal mortgage disbursed on or after October 1, 2011)

- PSLF

- Taxable Earnings-Pushed Reimbursement Forgiveness

Previous to consolidation, FFEL PLUS Loans are eligible for:

- Customary Reimbursement Plan

- Graduated Reimbursement Plan

- Prolonged Reimbursement Plan

- Earnings-Based mostly Reimbursement (IBR)

- Taxable Earnings-Pushed Reimbursement Forgiveness by way of IBR

After consolidation, FFEL Grad PLUS Loans are eligible for:

- The remaining Earnings-Pushed Reimbursement Plans: Revised Pay As You Earn (REPAYE), Earnings-Contingent Reimbursement (ICR), and PAYE (if borrowed after October 1, 2007 and have a federal mortgage disbursed on or after October 1, 2011)

- PSLF

- Taxable Earnings-Pushed Reimbursement Forgiveness by way of REPAYE, ICR, PAYE

Father or mother PLUS Loans

Father or mother PLUS Loans are issued to oldsters to finance their baby’s schooling. They’re provided for undergraduate, graduate, {and professional} diploma college students. Mother and father will normally take these loans if their baby is unable to cowl their tuition via federal scholar loans. Mother and father are responsible for the loans and finally chargeable for them.

Previous to consolidation, Father or mother PLUS Loans are solely eligible for:

- Customary Reimbursement Plan

- Graduated Reimbursement Plan

- Prolonged Reimbursement Plan

After consolidation, Father or mother PLUS Loans are eligible for:

- ICR

- Taxable Earnings-Pushed Reimbursement Forgiveness by way of ICR

- PSLF

To be eligible for extra IDR plans, you have to to do one other consolidation. One of these double consolidation wants cautious evaluate and is tough to get proper. We propose reserving a session with certainly one of our specialists.

Household Federal Schooling Mortgage (FFELP) Program

Earlier than 2010, the Household Federal Schooling Mortgage (FFELP) Program was the principle supply of federal scholar loans. This system resulted in 2010. Nearly all federal loans at the moment are issued beneath the Direct Mortgage program referred to above. However for many who nonetheless have these older loans, the next guidelines apply.

Previous to consolidation, FFELP Loans are eligible for:

- Customary Reimbursement Plan

- Graduated Reimbursement Plan

- Prolonged Reimbursement Plan

- IBR (to not be confused with IDR)

- Taxable Earnings-Pushed Reimbursement Forgiveness by way of IBR

After consolidation, FFELP Loans are eligible for:

- The remaining Earnings-Pushed Reimbursement Plans

- REPAYE, ICR (and PAYE if borrowed after October 1, 2007 and have a federal mortgage disbursed on or after October 1, 2011)

- PSLF

- Taxable Earnings-Pushed Reimbursement Forgiveness by way of REPAYE, ICR, PAYE

Perkins Loans

The Federal Perkins Scholar Mortgage Program was created to offer cash for faculty college students with decrease revenue or distinctive monetary want. This system ended on September 30, 2017.

Perkins Loans all have a 5% rate of interest, and they’re issued by the varsity you attend. They’re backed and received’t accrue curiosity whereas enrolled in class.

Perkins Loans aren’t eligible for quite a few federal packages, like Earnings-Pushed compensation (IDR) or public service mortgage forgiveness (PSLF), till they’re consolidated.

After consolidation, Perkins loans are eligible for:

- Customary Reimbursement Plan

- Graduated Reimbursement Plan

- Prolonged Reimbursement Plan

- All Earnings-Pushed Reimbursement Plans (and PAYE if borrowed after October 1, 2007 and have a federal mortgage disbursed on or after October 1, 2011)

- PSLF

- Taxable Earnings-Pushed Reimbursement Forgiveness

Evaluating Federal Scholar Loans

If you find yourself deciding which federal loans to decide on, you don’t have a lot discretion on which varieties of loans you’ll obtain. You’ll receive a mortgage provide from Federal Scholar Assist after you fill out the FASFA type offered by your faculty’s monetary assist workplace. On the undergraduate degree, you’ll obtain Direct Stafford backed and unsubsidized loans. There’s a cap on how a lot you may borrow in undergrad federally, and should you want extra loans, you’ll need to obtain Father or mother Plus Loans or seemingly apply for non-public scholar loans. Extra on borrowing thresholds later.

For graduate {and professional} diploma packages, the loans will encompass Direct Stafford unsubsidized loans and Direct Plus Graduate Loans. Direct Plus Graduate Loans are at all times issued at a 1% larger rate of interest than Direct Stafford unsubsidized loans. There isn’t any cap on how a lot you may borrow federally.

Household Federal Schooling Loans (FFELP) and Perkins Loans had been older-loan varieties that had been discontinued in 2010 and 2017, respectively. These loans are likely to have much less compensation plans and mortgage forgiveness choices than direct loans (Direct Stafford unsubsidized/backed and Direct Plus Graduate).

Every mortgage sort has completely different guidelines for compensation and mortgage forgiveness.

See the under chart to grasp extra of the nuances for every mortgage sort.

See our compensation or consolidation guides should you’d prefer to study extra about these matters.

Well being Assets and Companies Administration Loans

Other than the most typical federal scholar loans listed above, the Well being Assets and Companies Administration (HRSA) additionally points scholar loans completely to US healthcare professionals who show a monetary want pursuing their healthcare schooling. HRSA loans are need-based, and so they include service necessities which encourage debtors to apply in underserved communities. All of those loans are backed (authorities pays curiosity throughout faculty) and have a 5% mounted rate of interest. Every has its personal compensation phrases, forgiveness, and deferment eligibility.

Loans for Deprived College students (LDS)

Should pursue schooling as a doctor, dentist, optometrist, podiatrist, pharmacist or veterinarian. These loans could be deferred throughout residencies and internships. The compensation time period is 10 years, and the debt can develop into eligible for mortgage forgiveness via consolidation.

Major Care Mortgage

Should pursue an MD or DO program to be eligible and work in main care. If the borrower doesn’t work in main care, they are going to be positioned in service default and obtain penalty curiosity on the loans. These loans aren’t eligible to be consolidated to qualify for mortgage forgiveness.

Well being Professions Scholar Mortgage

These loans had been discontinued in 1993 and now fall beneath the Major Care Mortgage Program.

The right way to Apply for a Federal Scholar Mortgage

Your faculty’s web site or monetary assist workplace will direct you to the federal scholar assist type or FAFSA type to obtain scholar loans. After filling out the shape, federal scholar assist will give you particulars in your monetary assist package deal.

Previous to receiving federal scholar loans, you’ll full entrance counseling and signal a authorized doc referred to as a grasp promissory notice by which you promise to comply with the mortgage obligations. If in case you have further questions, contact your faculty’s monetary assist workplace.

What Are Federal Scholar Mortgage Curiosity Charges?

Federal scholar mortgage rates of interest observe rates of interest set by the Federal Reserve. Annually, they sometimes change as rates of interest fluctuate.

Curiosity Charges for Direct Scholar Loans July 1, 2022 to June 30, 2023

What Are Federal Scholar Mortgage Charges?

While you take out a federal mortgage, there’s a charge charged. The mortgage charge comes out of the cash paid to you when you’re nonetheless in class. So, the cash you obtain can be lower than the quantity you truly borrow.

Mortgage Charges for Direct Scholar Loans October 1, 2020 to September 31, 2023

Instance: Undergraduate borrower wants $5,000. They’re issued a mortgage of $5,287. $5,000 is the precise quantity which hits their checking account, however they owe $5,287. $287 is the mortgage charge. $5,000 * 1.057% = $5,287

How Is the Curiosity Calculated on Federal Scholar Loans?

Curiosity on federal scholar loans accrues every day, and it’s calculated as easy curiosity. (Mortgage principal stability * rate of interest) * numbers of days since final fee.

Does Curiosity Capitalize or Compound on Federal Scholar Loans?

Sure, curiosity can capitalize, and more often than not it’s unavoidable. Curiosity capitalization is when curiosity that has accrued in your loans will develop into principal, and your loans will begin rising off the next principal stability. Extra on curiosity capitalization.

The right way to Select Which Federal Scholar Mortgage?

While you borrow federally, you select how a lot you want, however aren’t capable of choose which mortgage sort. The mortgage sort provided will depend on how a lot you borrow and if it’s for undergraduate or graduate/skilled faculty.

Undergraduate Applications

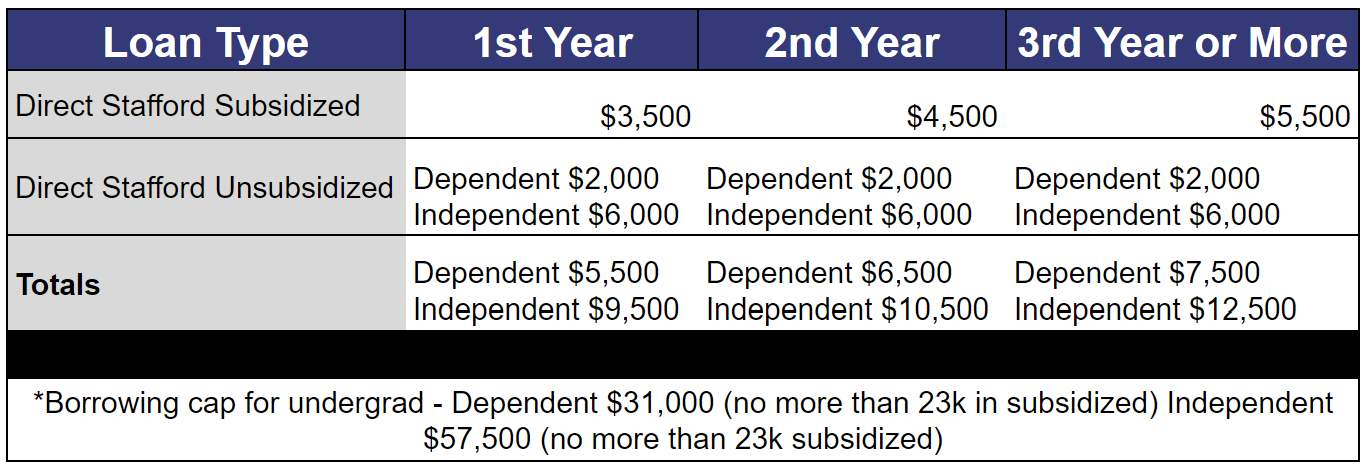

For undergraduate loans, there’s a cap on how a lot you may borrow. Additionally, your borrowing cap will depend on whether or not you’re a dependent or unbiased scholar. Dependent college students are assumed to have the assist of oldsters. Unbiased college students are not less than 24 years previous, married, in graduate/skilled faculty, within the armed forces, have kids, and so on. Mainly, in case your mother and father are going that will help you pay for college, you’re dependent. For those who’re by yourself paying for faculty, you’re unbiased.

Instance: If you’re an unbiased scholar in your first yr and also you borrow $5,000, the primary $3,500 can be backed and the remaining $1,500 can be unsubsidized. You might be mechanically first issued backed loans in undergrad.

For those who want greater than what’s provided federally, you may look into Father or mother Plus Loans or Personal Scholar Loans.

Graduate/Skilled Diploma Applications Non-Healthcare

The present cap for Direct Stafford unsubsidized is $20,500 per yr. For those who want further loans for the yr, the rest of your loans can be a Direct Plus Graduate Mortgage. For instance, you want $40,000 to pay for dental faculty tuition and afford to reside. Which means $20,500 can be issued as a Direct Stafford Unsubsidized Mortgage, and the remaining $19,500 can be a Graduate Plus Mortgage. Direct Stafford Sponsored Loans had been discontinued in 2012.

Graduate Skilled Applications Medical, Dental or different well being professions

These in graduate well being packages have the next borrowing threshold with Stafford loans, $20,500-$40,500. This can profit the borrower as a result of they are going to have the ability to take out extra Direct Stafford Loans earlier than they hit Direct Plus Graduate. Direct Plus Graduate are at all times issued 1% larger than Direct Stafford Loans.

Federal Scholar Mortgage Reimbursement Applications

There are a selection of federal compensation plans to contemplate when figuring out which compensation plan is finest for you. Customary, Graduated, and Prolonged compensation are based mostly in your mortgage quantity, size of compensation, and rate of interest. Earnings-Pushed Reimbursement relies in your revenue and family measurement.

Earlier than you start borrowing for college, take time to make a plan on the way to pay for it. First, apply for scholarships, grants and search for employment alternatives to cut back the price of faculty. After studying this information, should you’re nonetheless undecided on one of the best route, schedule a pre-debt seek the advice of.

Are you able to deal with your scholar loans?

Be a part of our group of docs, dentists and excessive earners. Every month you’ll get our FREE publication with all the information and methods that will help you save $$ in your scholar loans.

{kind=link}