Medical Scholar Loans: Your Full Information

It comes as no shock that medical doctors typically graduate from medical faculty with mortgage-sized pupil loans. Based on a research from the Affiliation of American Medical Faculties (AAMC), practically 73% of medical doctors reported having schooling debt. The median medical faculty mortgage stability for brand spanking new grads in 2020 was $200,000. However there are a lot of of you on the market strapped with a lot larger debt masses within the $300-$500k+ vary.

Med pupil mortgage debt is much more burdensome amongst youthful medical doctors, as tuition prices have continued to skyrocket over time. Sadly, wage will increase haven’t been commensurate with tuition will increase, placing some medical doctors in an much more precarious place with respect to their medical faculty mortgage debt.

Paying for medical faculty can get overwhelming shortly. There are federal loans and non-public loans with completely different guidelines, eligibility, and compensation plans. There’s non-public refinancing, consolidation, forbearance, and many others. Simply determining what these items means may require hours and hours of analysis poring over pupil mortgage literature. However don’t fear, SLA will help stroll you thru it.

If you happen to need assistance understanding the terminology, take a look at our Scholar Mortgage Phrases glossary.

Med pupil loans can impression a health care provider’s capacity to:

- Save for retirement

- Buy a house

- Get married or have youngsters

- Attend medical appointments

- Repay bank cards

- And way more

StudentLoanAdvice.com (SLA) was created to offer a third-party choice to assist medical doctors, dentists, and excessive earners lower your expenses on their pupil loans. Our workforce of pupil mortgage consultants have met with lots of of medical doctors making them a number of the most educated within the trade. The scholar mortgage panorama is rising extra advanced every day with a mess of compensation plans and mortgage forgiveness choices—every with various benefits and drawbacks which contact in your earnings, tax-filing standing, and even the way you’re contributing for retirement. It’s no shock that a lot of our shoppers, previous to our consultations, have been making five- and six-figure errors by means of mismanagement of their pupil loans.

For a number of hundred {dollars}, we’ll meet with you one-on-one, overview your state of affairs, and offer you a personalized pupil mortgage plan that will help you optimize your pupil mortgage administration.

This publish discusses a number of the fundamentals of pupil loans for medical faculty, compensation plans, and pupil mortgage debt forgiveness choices.

Desk of Contents:

How Do Scholar Loans Work for Medical Faculty?

Medical faculty pupil loans are issued to med college students to finance their schooling and related residing bills. They aren’t for use for every other objective. In contrast to a mortgage or auto mortgage, collectors don’t have any direct asset to grab when you default. As such, they are typically provided at charges considerably larger than mortgage charges, normally round 5%-8%.

Scholar loans are virtually by no means discharged in chapter. Nonetheless, generally they are going to be discharged attributable to demise or complete and everlasting incapacity. They may also be discharged in case your faculty closes earlier than you full your program or if the establishment defrauds you and different college students.

How A lot Scholar Mortgage Cash Ought to I Borrow for Medical Faculty?

Don’t borrow extra money than you want for medical faculty. Monetary assist places of work might suggest taking out further loans to cowl residing bills. If that is needful in your state of affairs, take out the least quantity essential to cowl your residing bills. A few of your folks might borrow greater than they should reside a lavish way of life on their loans. That is by no means a good suggestion.

Each greenback of mortgage cash you spend finally ends up costing you extra by the point you pay it again. Reside, however be conscious that the gallon of milk you simply purchased really price you $15 or the steak dinner actually price $300.

How Do I Obtain Medical Faculty Loans?

Your medical faculty’s web site or monetary assist workplace will direct you to the federal pupil assist type or FAFSA type to obtain pupil loans. After filling out the shape, federal pupil assist will offer you particulars in your monetary assist package deal.

Previous to receiving federal pupil loans, you’ll full entrance counseling and signal a authorized doc known as a grasp promissory word through which you promise to comply with the mortgage obligations. When you have further questions, contact your faculty’s monetary assist workplace.

Monetary assist places of work might supply different varieties of federal and non-federal loans nevertheless it varies by establishment. Study extra about non-federal loans beneath.

Mortgage Corporations for Medical Faculty

Scholar mortgage lenders are normally the federal government, a faculty, or a non-public lender. If you happen to apply on FAFSA for a pupil mortgage, you’ll obtain a pupil mortgage from the federal authorities. At present, nearly all of federal pupil loans are known as direct federal pupil loans. Studentaid.gov is the house web site the place they’ve your entire mortgage info.

Your med faculty can lend to you straight by means of institutional loans and/or Perkins loans. These loans aren’t as frequent as direct federal pupil loans or non-public loans issued by non-public lenders.

If you wish to obtain further loans, you’ll must contact a non-public lender. A non-public lender is often a financial institution or monetary establishment that may difficulty loans for schooling. Personal loans have much less flexibility and protections than federal loans.

Though federal loans come from the federal authorities, it sometimes outsources the mortgage servicing. Mortgage servicers handle the day-to-day elements of your mortgage funds. In contrast to federal loans, non-public lenders will sometimes difficulty and repair your pupil loans.

What Is a Scholar Mortgage Servicer?

A pupil mortgage servicer oversees the administration of your pupil loans. Your servicer will hold monitor of your month-to-month funds, forgiveness credit, late funds, relevant tax varieties, fee historical past, and many others. Periodically, your pupil mortgage servicer can change. You’ll be informed through e mail or snail mail when this occurs. Ensure you log in commonly to make sure your contact info is updated.

Paying for Medical Faculty: Federal vs. Personal Scholar Loans

Every time potential, we suggest you are taking out federal pupil loans earlier than non-public loans when paying for medical faculty. There isn’t a restrict on how a lot you’ll be able to borrow federally for medical faculty. As well as, federal pupil loans are likely to have decrease rates of interest initially and a plethora of federal protections that non-public pupil loans don’t supply. Comparable to:

- Earnings-Pushed Reimbursement (IDR) – fee primarily based on earnings

- Public Service Mortgage Forgiveness (PSLF) – 10-year tax-free mortgage forgiveness

- Taxable Earnings-Pushed Reimbursement Forgiveness – 20-25 yr taxable mortgage forgiveness

- Loss of life and Incapacity Discharge – pupil loans are discharged tax-free within the occasion of demise or complete and full incapacity

- Forbearance – briefly placing federal pupil mortgage funds on maintain whereas non-public loans supply little to no flexibility when you can’t make your funds

Federal Scholar Loans

Federal pupil loans are the commonest sort of loans med college students borrow to finance their schooling. They arrive with a wide range of mortgage varieties, compensation plans, and mortgage forgiveness choices. Most US medical colleges will qualify for federal pupil loans, however for many who attend medical faculty exterior of the US will most definitely need to look to the non-public sector for pupil loans.

Sponsored vs. Unsubsidized Federal Scholar Loans

Sponsored federal pupil loans don’t develop or accrue curiosity when you are in class. Sponsored loans have been discontinued for medical faculty packages in 2012, and they’re now solely provided on the undergraduate stage. Those that attend medical faculty now or who’re planning to attend should make the most of unsubsidized loans. These loans start accruing curiosity the second you obtain them.

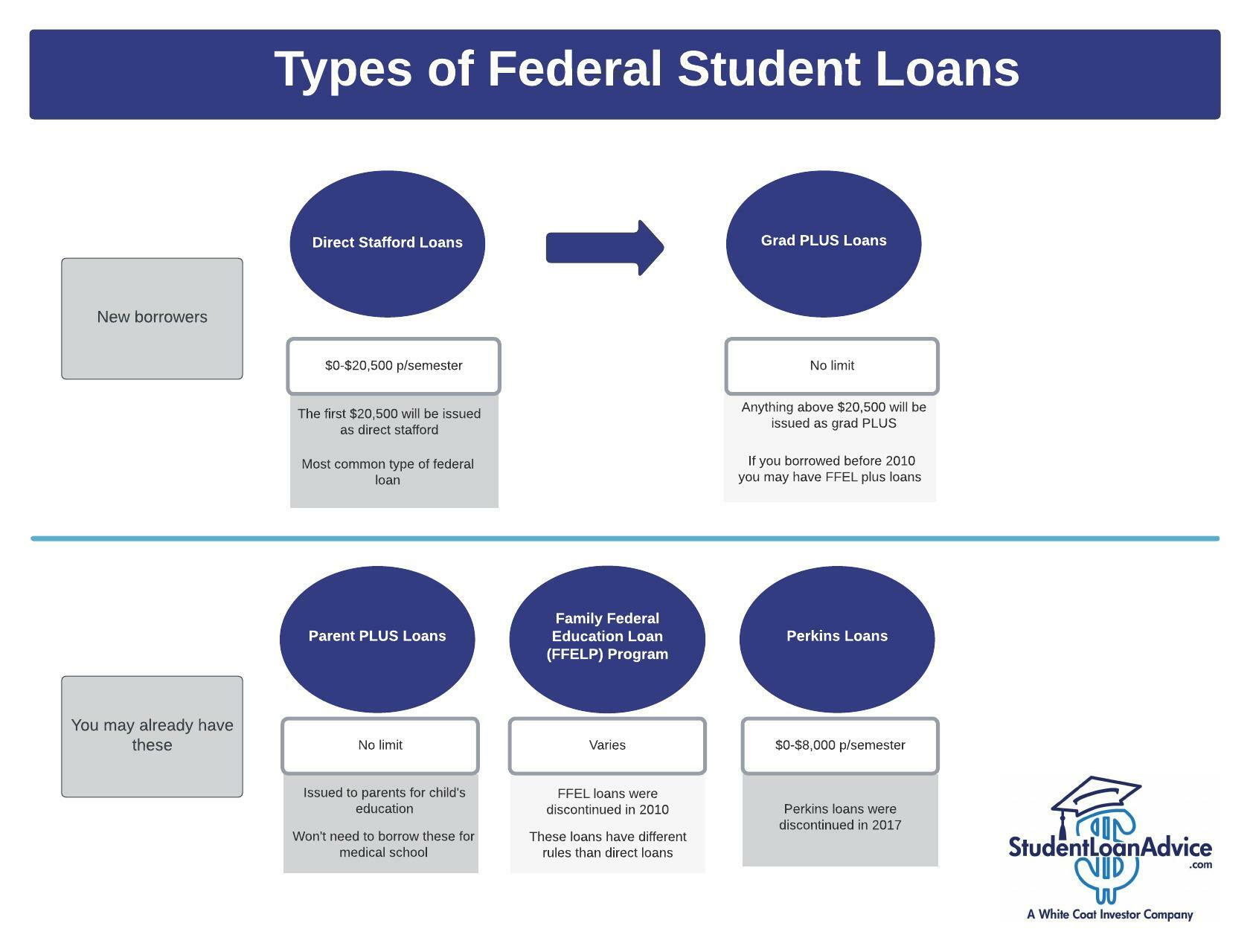

Varieties of Federal Scholar Loans

There are 5 fundamental varieties of federal pupil loans to think about.

New debtors primarily want to grasp two mortgage varieties, direct Stafford loans and grad PLUS loans. If you end up borrowing for medical faculty the primary $20,500 per semester might be direct Stafford loans. If you happen to want loans above that quantity they are going to difficulty you grad PLUS loans. Grad PLUS loans are issued with a better rate of interest and mortgage charges than direct Stafford loans. Grad PLUS loans don’t have any borrowing cap. Those that have already borrowed for medical faculty (and for different education) possible have a mixture of the beneath mortgage varieties.

Direct Stafford Loans

Stafford Loans originated from the William D. Ford Federal Direct Mortgage (Direct Mortgage) Program. Direct Stafford Loans are the commonest pupil loans and are presently being issued to assist cowl the price of larger schooling.

Grad PLUS Loans

Grad PLUS Loans, aka Graduate PLUS Loans, come from the Direct and Household Federal Schooling Mortgage (FFELP) packages. Debtors are issued these loans to cowl tuition after exhausting Stafford Loans.

Guardian PLUS Loans

Guardian PLUS Loans are issued to oldsters to finance their youngster’s schooling. They’re provided for undergraduate, graduate, {and professional} diploma college students. Mother and father will normally take out these loans if their youngster can’t cowl their tuition by means of federal pupil loans. Mother and father are answerable for the loans and in the end chargeable for them. There isn’t a cap on federal borrowing for graduate {and professional} diploma packages so that you shouldn’t ever have to make use of these when borrowing for medical faculty.

Household Federal Schooling Mortgage (FFELP) Program

Earlier than 2010, the Household Federal Schooling Mortgage (FFELP) Program was the principle supply of federal pupil loans. This system led to 2010, and it’s now defunct. Nearly all federal loans are actually issued underneath the Direct Mortgage program referred to above. However for many who nonetheless have these older loans, there are completely different guidelines relevant to this mortgage program.

Perkins Loans

The Federal Perkins Scholar Mortgage program was created to offer cash for faculty college students with decrease earnings or distinctive monetary want. This system ended on September 30, 2017.

Perkins Loans all have a 5% rate of interest and are issued by the varsity you attend. They’re sponsored and gained’t accrue curiosity whereas enrolled in class.

Well being Sources and Providers Administration Loans (HRSA)

Other than the commonest federal pupil loans listed above, the Well being Sources and Providers Administration (HRSA) additionally points pupil loans completely to US healthcare professionals who display a monetary want pursuing their healthcare schooling. HRSA loans are need-based and include service necessities which encourage debtors to follow in underserved communities. All of those loans are sponsored (authorities pays curiosity throughout faculty) and have a 5% fastened rate of interest. Every has its personal compensation phrases, forgiveness, and deferment eligibility.

Federal Reimbursement Packages

There are a selection of federal compensation plans to think about when figuring out which compensation plan is finest for you. Commonplace, Graduated, and Prolonged compensation are primarily based in your mortgage quantity, size of compensation, and rate of interest. Earnings-Pushed Reimbursement is predicated in your earnings and family measurement.

- Commonplace Reimbursement Plan – fastened funds over 10 years

- Graduated Reimbursement Plan – funds begin at a decrease quantity and improve each two years at a charge to repay the mortgage over 10 years

- Prolonged Reimbursement Plan – fastened funds over 25 years

- Earnings-Pushed Reimbursement (IDR) Plans – funds are calculated as a proportion of discretionary earnings. IDR plans are a requirement for Public Service Mortgage Forgiveness (PSLF).

Extra on Federal Scholar Mortgage Reimbursement Packages

Methods to Enroll right into a Federal Reimbursement Plan

Your mortgage servicer will ship you a notification to enroll right into a compensation plan whenever you graduate. If you happen to don’t choose a plan, you’ll be in the usual 10-year plan. If you happen to’d wish to be positioned within the graduated or prolonged compensation plan, name your mortgage servicer and request to be positioned on that plan.

Most debtors with federal loans ought to enroll into an IDR plan. REPAYE or PAYE are the very best IDR plans. You might also want to think about Previous IBR and ICR. If you happen to’d wish to enter an IDR plan, you’ll must fill out an Earnings-Pushed Reimbursement Utility type. There’s an digital and paper type software.

If you happen to’d like help with selecting a compensation plan, schedule an appointment with a pupil mortgage professional.

How A lot Will My Scholar Mortgage Fee Be?

Your pupil mortgage fee can rely upon a wide range of elements, corresponding to your compensation plan, earnings, family measurement, tax submitting standing, and many others. Right here’s a calculator that will help you learn how a lot your fee can be.

Bonus Tip: There are a selection of Federal Scholar Mortgage Statuses you want to pay attention to to make sure you don’t pay further in the long term or eradicate the chance for forgiveness.

How Do I Decrease My Month-to-month Fee on Medical Faculty Loans?

Funds on loans for medical faculty might be lowered in plenty of methods for each federal and personal pupil loans.

Federal Scholar Loans

-Enroll in an Earnings-Pushed Reimbursement (IDR) plan as a substitute of the usual 10-year, graduated or prolonged compensation plan.

-Personal refinance your federal pupil loans right into a decrease rate of interest. Usually, this could offer you a decrease fee.

Personal Scholar Loans

-Lengthen your mortgage time period.

-Personal refinance your loans to a decrease rate of interest.

-Add a co-signer with sturdy credit score whenever you non-public refinance your pupil loans. Word, the co-signer turns into collectively answerable for the debt in the event that they co-sign.

Strategies to cut back month-to-month funds in Earnings-Pushed Reimbursement Plans

-Contribute to pre-tax accounts, corresponding to a 401(ok), 403(b), 457, TSP, Well being Saving Account (HSA), and Versatile Spending Account (FSA).

-File taxes as a pair married submitting individually (MFS)—be taught extra about this technique right here.

Personal Scholar Loans for Medical Faculty

Personal Scholar Loans are sometimes taken out by college students who’ve maxed out their federal borrowing restrict for the yr when borrowing for undergrad. With graduate {and professional} diploma packages, there isn’t any cap on federal borrowing. Federal pupil loans ought to at all times be taken out earlier than non-public.

Eligibility Necessities for Personal Scholar Loans

Most debtors will obtain non-public pupil loans from a non-public lender. If you happen to resolve to take out a non-public pupil mortgage, an underwriter will take a look at your credit score rating, debt-to-income ratio, financial savings, and job historical past to find out your creditworthiness. Most have to be a US citizen, everlasting resident, or have a co-signer who’s. Additionally, you should be of authorized age to borrow. This varies by state.

Personal Scholar Mortgage Reimbursement Plans

There are 4 fundamental methods to repay your non-public pupil loans. Be suggested: the longer your fee time period, the extra curiosity you’ll find yourself paying.

- Rapid Reimbursement – month-to-month funds start primarily based on a five-, 10-, 15-, or 20-year time period. That is the bottom price choice of the 4 compensation choices.

- Curiosity-Solely – month-to-month funds solely masking the curiosity.

- Partial – typically an choice for many who are nonetheless in class or coaching who want to make a low fastened fee. Word, this is quite common throughout coaching.

- Full Deferment – not required to make funds in class, nevertheless it’s the costliest choice of the 4.

Extra on Personal Mortgage Reimbursement and which choice to decide on

Scholar Mortgage Administration for Docs

For many medical doctors, it is strongly recommended to think about mortgage forgiveness or non-public refinancing. Happening both of those routes is extra advantageous than sticking with a typical, graduated, or prolonged compensation for federal pupil loans. If you’re contemplating mortgage forgiveness, you’ll most definitely want to think about federal pupil mortgage consolidation. Skip this part when you simply plan on non-public refinancing.

Federal Scholar Mortgage Consolidation

Federal pupil loans might be consolidated. Throughout this course of, quite a few loans are all lumped collectively into one mortgage (or two in some instances), and the rates of interest are averaged after which rounded as much as the closest 1/eighth of a p.c. That is distinct and completely different from the method of personal refinancing, the place the rate of interest is mostly lowered and loans are transformed from federal to non-public.

Financially, generally the benefit of finishing a direct federal consolidation is that it makes you eligible for various compensation plans and forgiveness choices. If you happen to’re a brand new grad or quickly might be, a direct federal consolidation can will let you choose out of the automated six-month grace interval that you just’ll enter whenever you graduate. This is able to will let you begin paying your loans sooner and start credit score to mortgage forgiveness earlier.

Please word: whenever you full a consolidation, it’s going to erase your prior fee historical past in your mortgage(s). This is a vital consideration when you’re doing mortgage forgiveness. This rule might be modified starting July 1st, 2023. Once you consolidate your direct pupil loans, they are going to take a weighted common of present qualifying funds towards PSLF. Right here’s an instance underneath the proposed guidelines: say you might have 100k of loans at 90 months and 100k of loans at 30 months. If you happen to consolidate them you’d have a brand new qualifying fee rely of 60 on your entire loans.

Scholar Mortgage Forgiveness for Docs

Most pupil mortgage forgiveness packages that medical doctors ought to contemplate are for federal pupil loans.

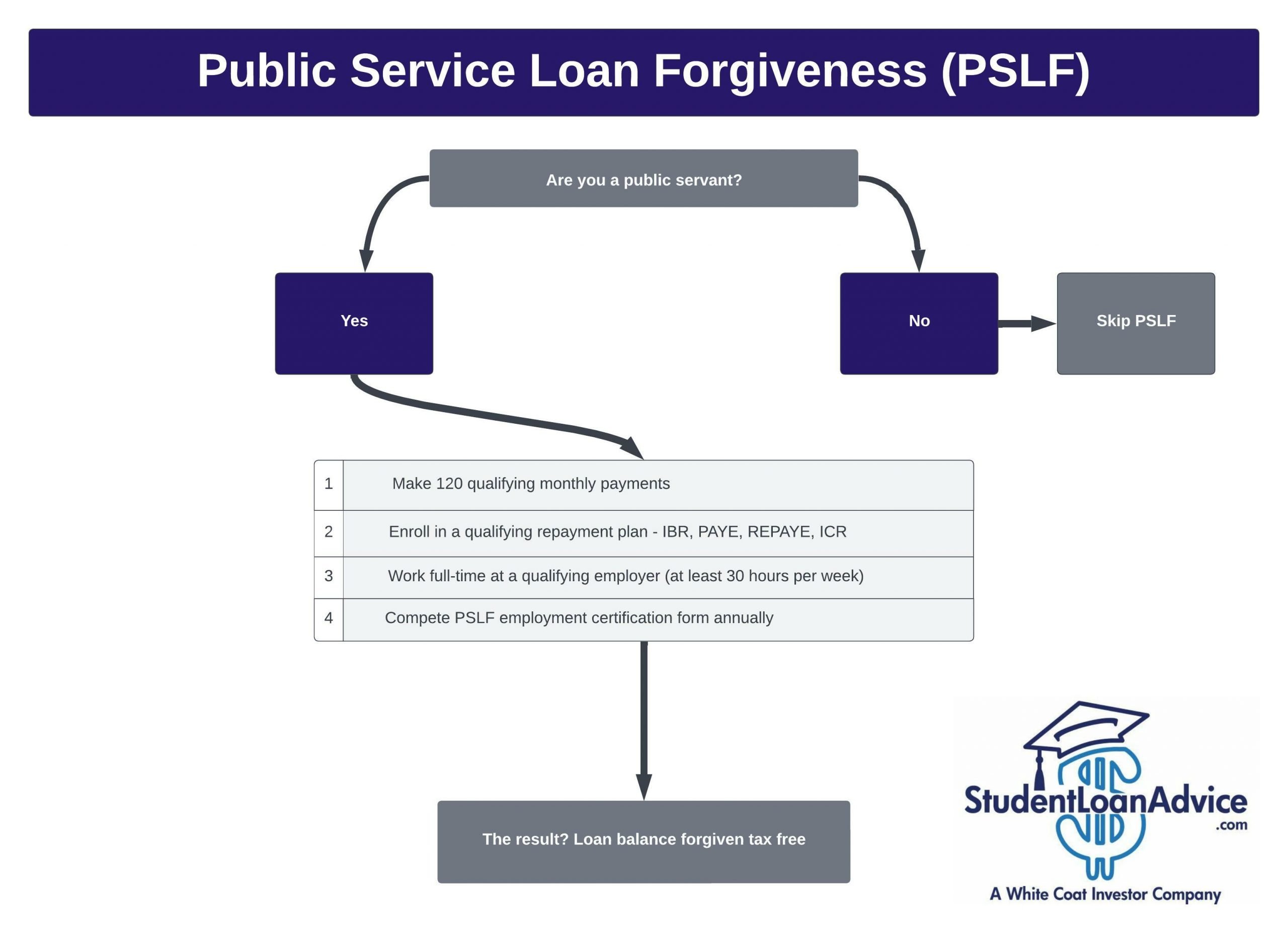

Public Service Mortgage Forgiveness (PSLF)

Public Service Mortgage Forgiveness or PSLF is the very best mortgage forgiveness program on the market. If you happen to qualify, you must positively contemplate it.

Who Is Eligible for PSLF?

Typically talking, any borrower is eligible who works for a nonprofit group or for the federal government. Use the PSLF assist device to find out in case your employer qualifies.

What Varieties of Loans Are Eligible for Forgiveness?

Direct federal loans (unsubsidized and sponsored), direct graduate PLUS, and direct consolidation loans are eligible for PSLF.

What Are the Necessities of PSLF Mortgage Forgiveness?

- Make 120 qualifying month-to-month funds. These are cumulative funds, not consecutive.

- Enroll in a qualifying compensation plan—IBR, PAYE, REPAYE, ICR, or the usual 10-year compensation. Word: when you enroll in the usual 10-year fee plan and make funds for 10 years, there might be nothing left to forgive.

- Work full-time at a qualifying employer or the equal of full-time throughout a number of companies or organizations (not less than 30 hours p/wk). Certified employers are typically the federal government and nonprofits. Watch out as employers will generally be for-profit however affiliated with a authorities or nonprofit entity. FMLA will rely when you don’t take greater than 12 weeks and proceed to make month-to-month funds.

- Have direct federal pupil loans, as talked about above.

- Submit a PSLF certification type to confirm your employment at a certified employer and hold monitor of funds. It’s advisable to submit this kind not less than yearly to assist servicers hold monitor of funds. A residency program director, fellowship director, HR supervisor, and many others., would be capable of signal it.

How A lot Can Docs Have Forgiven By PSLF?

Any excellent mortgage quantity (principal and curiosity) might be forgiven tax-free after you might have accomplished 120 qualifying funds. You’ll obtain a refund when you’ve paid greater than 120 funds on direct loans.

Please word that you want to be extraordinarily meticulous together with your record-keeping and guarantee your mortgage servicer is appropriately categorizing (or counting) every of your month-to-month funds. Finishing the PSLF certification type yearly is one of the best ways to mitigate your servicer’s errors. Your servicer will possible make errors in your software, and also you’ll must appropriate them.

How Lengthy Does It Take to Have Loans Forgiven By PSLF?

PSLF takes about 10 years to finish.

Please word: There’s a short-term rest of plenty of these necessities. Examine it right here.

Taxable Earnings-Pushed Reimbursement Forgiveness

Taxable Earnings-Pushed Reimbursement Forgiveness is an alternative choice for medical doctors who’re ineligible for PSLF and have pupil mortgage debt 3, 4 or 5x+ their earnings. We virtually by no means suggest any doc pursue this program. If you happen to’re a health care provider who doesn’t qualify for PSLF however has large quantities of debt and is contemplating this forgiveness program, schedule a time with an expert at SLA.

Who Is Eligible for Taxable Earnings-Pushed Reimbursement Forgiveness?

Debtors enrolled in income-driven compensation packages are eligible.

What Varieties of Loans Are Eligible?

Direct federal loans (unsubsidized and sponsored), direct consolidation loans, Guardian PLUS loans if consolidated (ICR solely), and FFEL loans.

What Are the Necessities?

Be enrolled in an income-driven compensation program. Make month-to-month funds. Full the annual income-driven compensation (IDR) certification.

How A lot Might Be Forgiven?

The excellent mortgage quantity might be forgiven after you might have accomplished the fee time period. The forgiven quantity might be taxed for debtors receiving this forgiveness after 2025. The taxed forgiven quantity is also known as the “tax bomb” as a result of the taxes paid within the yr the loans are forgiven might be large. The tax bomb makes this program a lot much less interesting until you save up for it alongside the best way. Arrange a facet fund to organize for the tax bomb. That is an account the place, periodically (typically suggested month-to-month), you’ll contribute cash to an funding account of your option to put aside sufficient cash to pay the tax invoice within the yr your federal loans are forgiven.

How Lengthy Does Taxable Earnings-Pushed Reimbursement Forgiveness Take?

- REPAYE – 20 years for undergrad, 25 years for graduate.

- PAYE – 20 years.

- IBR – 25 years (20 years for debtors who took out loans after July 1, 2014).

- ICR – 25 years.

If you happen to’d wish to discover further forgiveness choices, please see our publish on Scholar Mortgage Forgiveness Packages.

Refinance Medical Faculty Loans

The aim of refinancing medical faculty loans is to decrease the rate of interest in your pupil loans and to pay much less curiosity. You’ll be able to refinance federal and personal pupil loans collectively.

Federal Scholar Loans

If you happen to’ve determined pupil mortgage forgiveness isn’t best for you, you must positively contemplate non-public refinancing. Don’t maintain on to these excessive federal pupil mortgage rates of interest (6%-8%) longer than wanted.

Right here’s an instance of two medical doctors:

Physician 1: med pupil loans 200K, rate of interest 7%, 10-year time period

Physician 2: med pupil loans 200K, rate of interest 3%, 10-year time period

Physician 2 made decrease month-to-month funds and, in complete, paid $46,914 much less in curiosity

Personal Scholar Loans

Anytime you’ll be able to obtain a decrease rate of interest by non-public refinancing, it is strongly recommended you accomplish that to pay the minimal quantity on curiosity. Personal lenders will take a look at your credit score, job historical past, earnings, financial savings, and debt. The higher you’re in every of those classes, the higher charge you’ll typically obtain. Be certain to take a look at charges throughout these inflection factors in your profession.

- Medical faculty commencement to resident

- Resident to attending doctor

- Make accomplice in your follow

- Marriage to a different earner

Mortgage Reimbursement Help Packages (LRAPs)

Mortgage compensation help packages (LRAPs) are packages which assist pay down your federal and personal pupil loans. There are lots of LRAPs obtainable to debtors when you work in particular states, be a part of the army, work in a high-need space, and way more.

See our information on LRAPs to be taught extra.

Conclusion

In case your head is spinning after studying by means of this information, you’re not alone. This was the case once we first discovered about these items, too. It’s tough and nuanced, and it may be tense when deciding how finest to handle your pupil loans. This explains why we regularly establish five- or six-figure errors our shoppers have been making previous to their session with us.

Schedule your session with us at StudentLoanAdvice.com, and also you’ll obtain a personalized pupil mortgage plan that may prevent hours of analysis and stress and doubtlessly hundreds of {dollars}. Begin down the trail towards monetary independence by letting us information you thru your finest pupil mortgage choices.

Are you able to sort out your pupil loans?

Be a part of our group of medical doctors, dentists and excessive earners. Every month you’ll get our FREE publication with all the ideas and methods that will help you save $$ in your pupil loans.

{kind=link}